If you had invested ₹1 lakh in Paytm's IPO in 2021, your money would be worth roughly ₹54,000 today. That is not a bad quarter. That is not bad luck. That is a system that allowed overpriced stories to be sold to ordinary Indians at extraordinary prices.

India's IPO market in the last decade has been a tale of two realities. On one side, some listings genuinely created wealth. On the other side, a handful of high-profile IPOs destroyed crores of rupees of hard-earned retail money — and the stories behind them are mostly similar every single time.

This article breaks down the worst IPOs in India's recent history, explains exactly why they failed investors, and gives you the lessons that most financial advisors will never tell you plainly.

Why Do Indian IPOs Fail So Badly?

Before we name names, let us understand the pattern. In almost every major IPO disaster in India, the destruction happened due to the same four reasons:

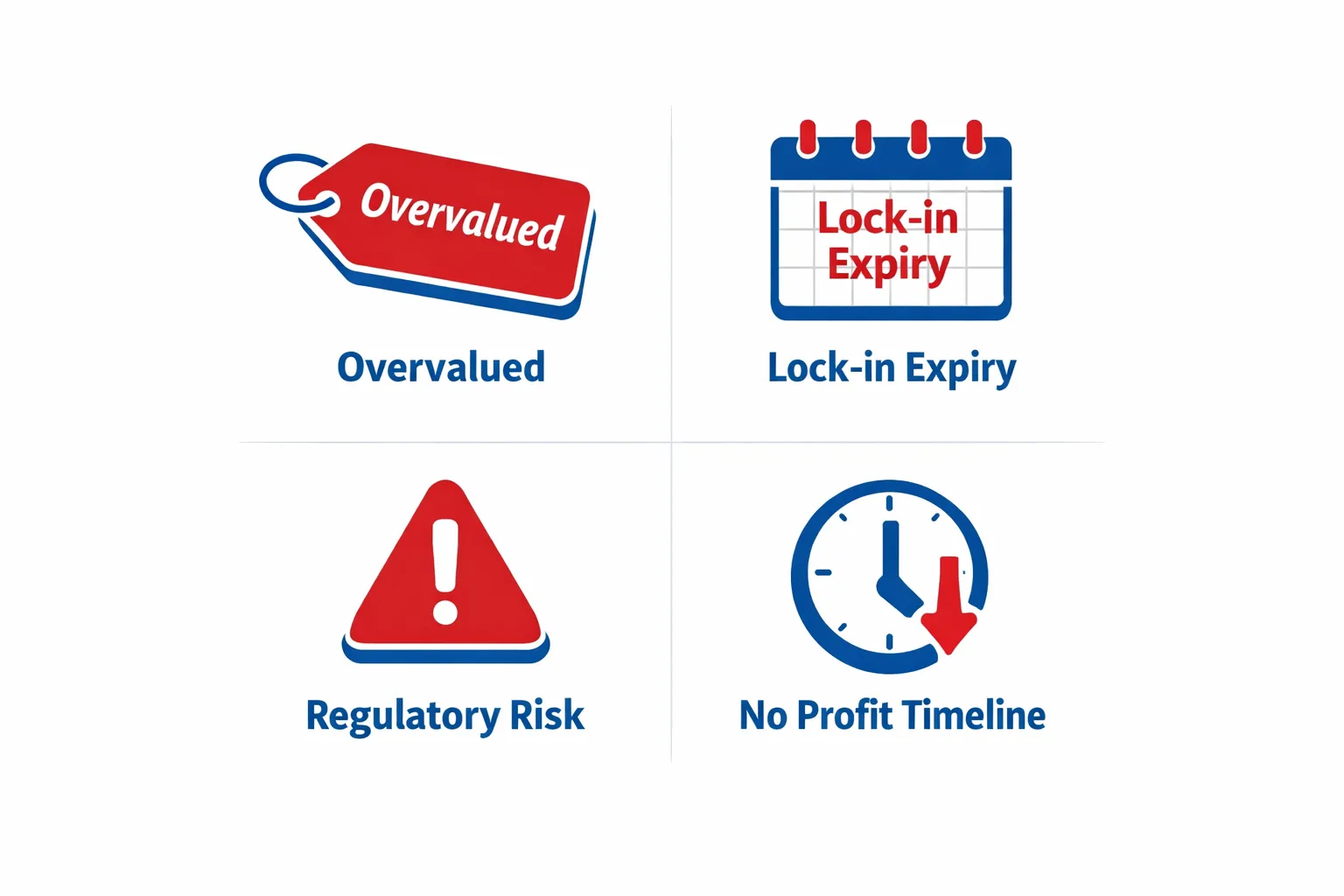

First, the valuation at IPO was simply too high. The company was priced for perfection — assuming years of future growth had already happened.

Second, large early investors (promoters, PE funds, anchor investors) sold their shares the moment their lock-in period ended, flooding the market with supply.

Third, regulatory or operational shocks hit the company after listing, when retail investors were already holding the bag.

Fourth, the promised path to profits kept getting delayed, quarter after quarter, until the market simply gave up.

Remember this: IPO losses are rarely about one bad quarter. They are about mispriced certainty. When that certainty breaks, the stock re-rates downward very fast — and retail investors feel the full pain.

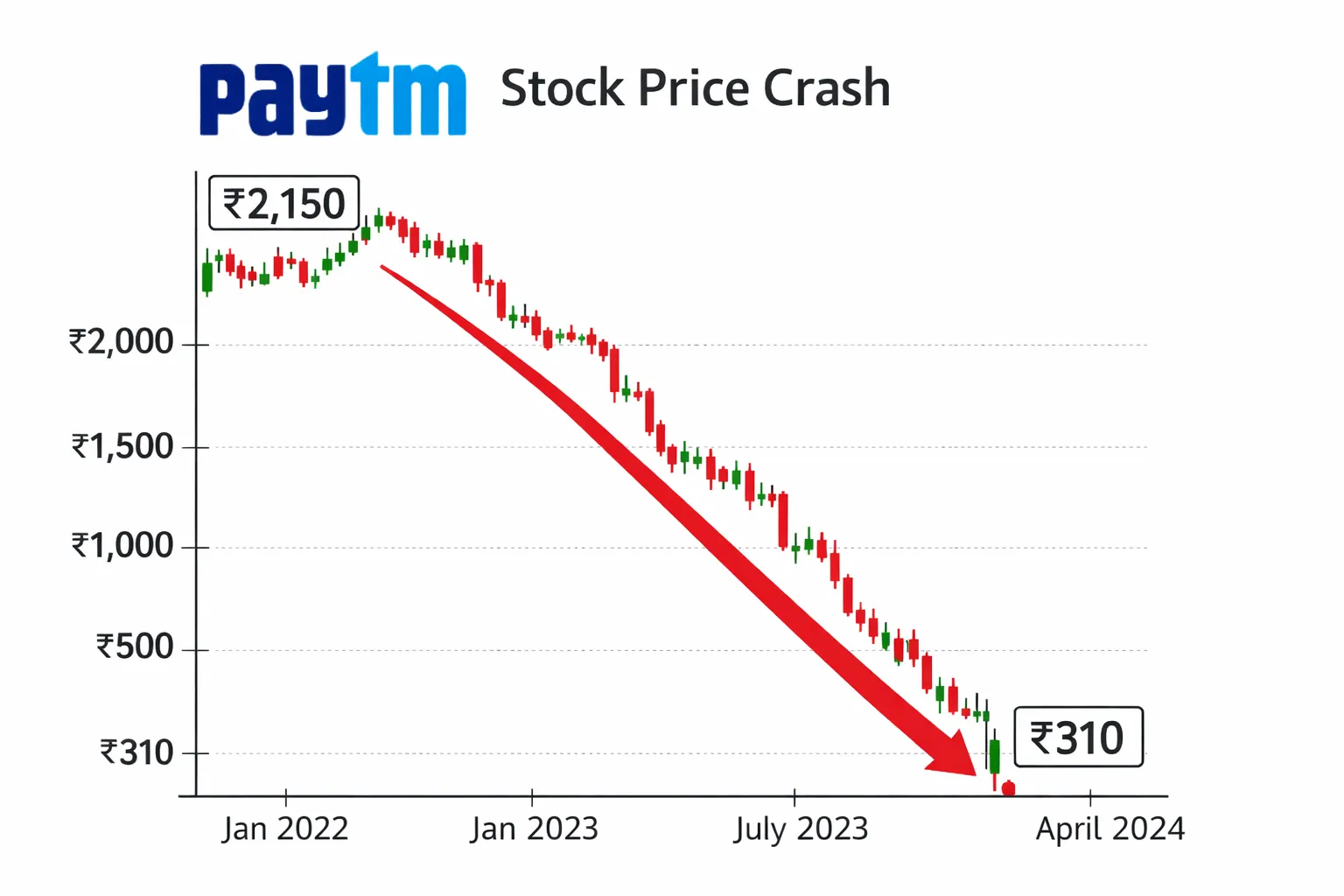

1. One97 Communications (Paytm) — India's Most Infamous IPO Disaster

Issue Price: ₹2,150

Listing Price: ₹1,950 (NSE)

All-Time Low: ₹310

Current Price (Feb 2026): ~₹1,157

Loss from Issue Price: ~46%

Loss from Peak: ~84%

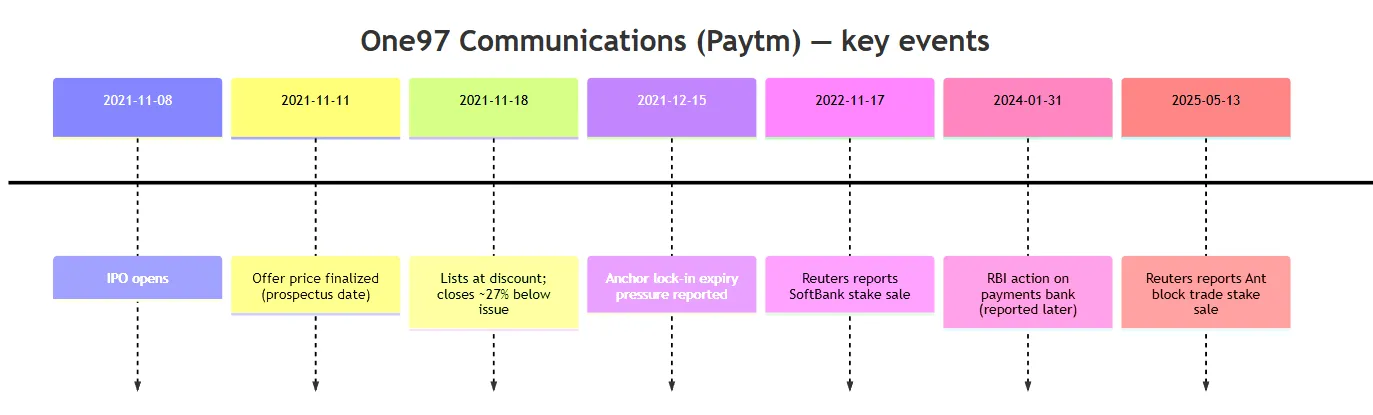

Paytm's November 2021 IPO was the largest in Indian history at that time — ₹18,300 crore raised. The hype was unreal. But within minutes of listing, the stock fell below its issue price and closed almost 27% down on day one.

What happened next was textbook wealth destruction. The 30-day anchor lock-in expired and institutional holders started selling. Large shareholders like SoftBank and Ant Group began reducing their stakes through block trades — one after another, year after year. Then in January 2024, the RBI ordered the wind-down of Paytm Payments Bank citing compliance issues, and the stock absolutely collapsed.

The company was burning cash at the time of its IPO. It was priced as if it was already profitable — or would become profitable very soon. It was neither. Retail investors who trusted the brand paid the price.

What you should have seen: The prospectus clearly mentioned that anchor investors were locked in for only 30 days and pre-offer capital for one year. That is a very short window. When a stock is already weak at listing, lock-in expiry becomes a guaranteed supply shock. Calendar those dates. Always.

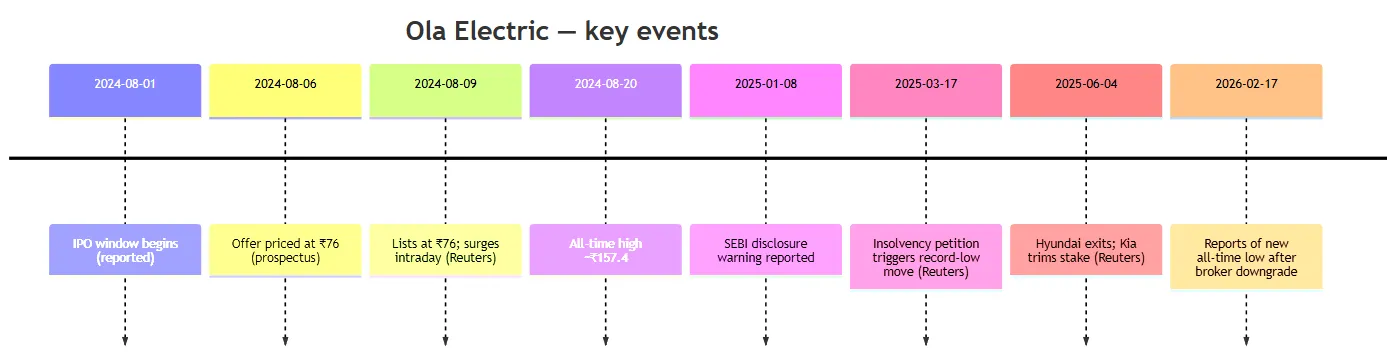

2. Ola Electric Mobility — The EV Dream That Turned Into a Nightmare

Issue Price: ₹76

All-Time High: ₹157.40 (August 2024)

All-Time Low: ₹27.36 (February 2026)

Current Price (Feb 2026): ~₹27.51

Loss from Issue Price: ~64%

Loss from Peak: ~83%

Ola Electric listed in August 2024 and for a brief moment, everything looked perfect. The stock debuted at ₹76, hit the upper circuit, and touched ₹157 within days. The EV revolution was here. India's future was now.

Then reality arrived.

SEBI issued a warning related to disclosure timing — Ola was making announcements on social media before officially filing with the exchanges. That kind of governance issue, small as it may seem, is a big red flag for a newly listed company. Hyundai eventually sold its entire stake. Kia trimmed its holding. SoftBank quietly reduced its position over time.

By March 2025, there were reports of an insolvency petition filed against one of Ola's units. Sales were shrinking. Losses continued. The stock hit new lows repeatedly. By February 2026, it was trading near its all-time low of ₹27 — roughly one-third of its IPO price.

What you should have seen: Ola's lock-in structure had staged releases — six months for pre-offer capital, and a split 90-day and 30-day window for anchor investors. Staged lock-in means staged supply. When a stock has already peaked and fundamentals are weak, each unlock is another wave of selling pressure.

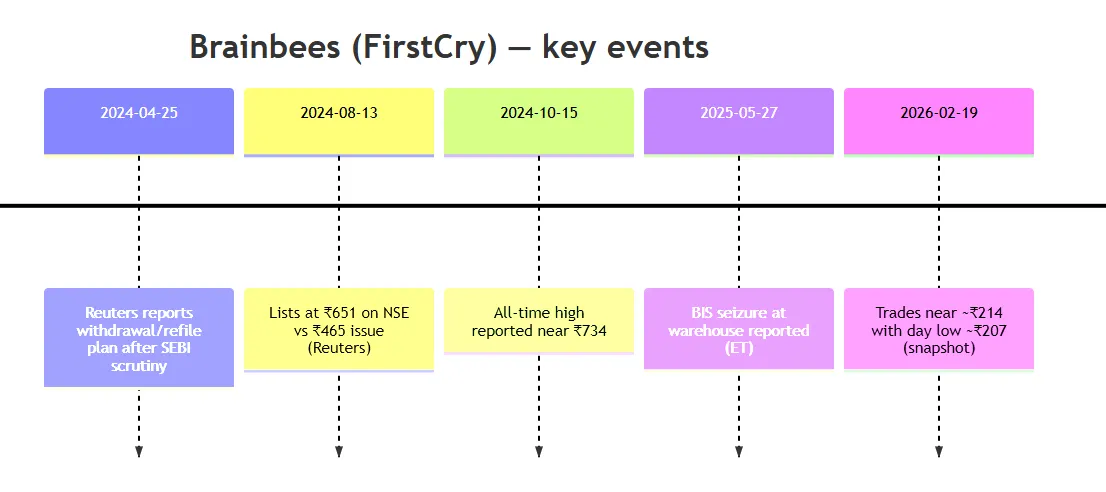

3. Brainbees Solutions (FirstCry) — Great Debut, Painful Journey

Issue Price: ₹465

Listing Price: ₹651 (NSE)

All-Time High: ₹734 (October 2024)

Current Price (Feb 2026): ~₹214

Loss from Issue Price: ~54%

FirstCry had a genuinely exciting debut. It listed 40% above its issue price, making early applicants feel like geniuses. But what followed was a slow, painful grind downward.

Before its IPO, SEBI had raised questions about how the company was disclosing certain business metrics — and FirstCry had to withdraw and refile its IPO papers. That should have been a warning sign about how the business was presenting its numbers.

Post-listing, a BIS search-and-seizure action at one of FirstCry's warehouses was disclosed through an exchange filing. For a consumer brand that depends on parent trust, compliance incidents are not just legal problems — they are brand problems. And brand problems become valuation problems.

Major backers like SoftBank, TPG, and Mahindra & Mahindra were listed as key investors. When funds of that size are sitting on IPO-era shares, the question is always: at what point do they exit? That exit pressure never truly goes away until the lock-in calendar is fully over.

What you should have seen: A great listing day can create false confidence. The fundamental question is always: what is the realistic path to sustained profitability? For FirstCry, that path remained blurry, and the market eventually priced that uncertainty in.

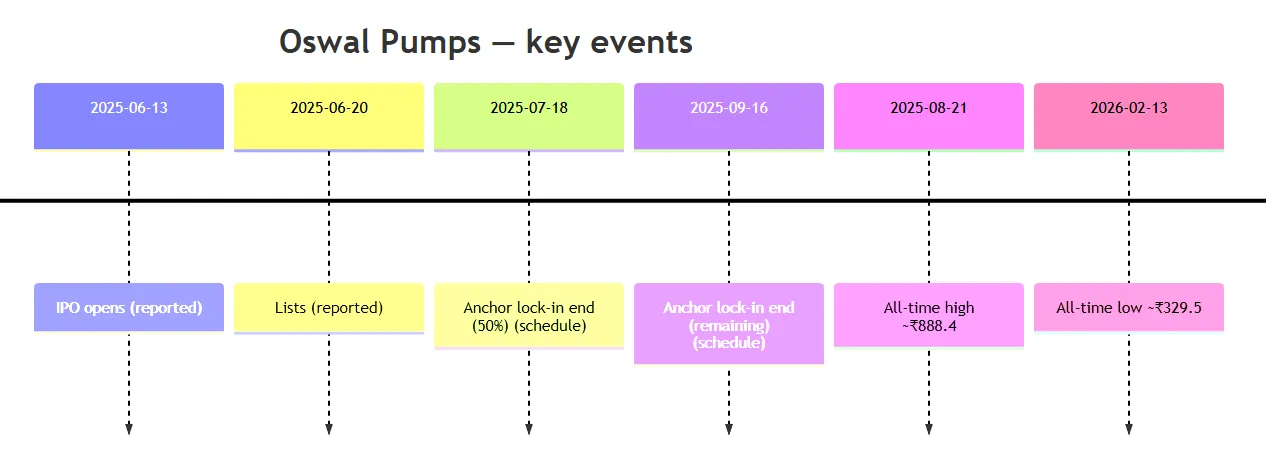

4. Oswal Pumps — Small IPO, Big Hype, Bigger Fall

Issue Price: ₹614

Listing Price: ₹634

All-Time High: ₹888.40 (August 2025)

All-Time Low: ₹329.50 (February 2026)

Current Price (Feb 2026): ~₹341

Loss from Issue Price: ~44%

Oswal Pumps is a smaller issue, but it is a perfect example of what happens in mid-and-small cap IPOs when momentum buyers enter without checking fundamentals.

The stock listed modestly, then doubled to nearly ₹888. That kind of move attracts retail buyers who think they missed the rally and want to get in before it goes higher. Then the anchor lock-in windows opened — 50% at one date, the rest at another — and supply started flooding a stock with a small free float. By February 2026, it had fallen to ₹329, well below its issue price.

There was no single dramatic news event here. Just the normal mechanics of supply and demand, playing out in a stock where liquidity was thin and the fundamentals could not justify the peak valuation.

What you should have seen: The anchor lock-in expiry dates were publicly available in the IPO schedule. Any retail investor could have calendared those dates. When a small-float stock has run up 40% from issue price, and a big supply unlock is coming in a few weeks — that is your signal to be careful.

5. Seshaasai Technologies — Flat Listing, Then a Straight Fall

Issue Price: ₹423

Listing Price: ₹432 (NSE)

All-Time High: ₹437.45 (September 2025 — essentially listing day)

All-Time Low: ₹231.05 (January 2026)

Current Price (Feb 2026): ~₹249

Loss from Issue Price: ~41%

Seshaasai Technologies listed at a small premium and then almost immediately started falling. The all-time high was achieved on or around listing day itself — meaning the stock never found new buyers willing to pay more than what IPO applicants had already paid.

Valuation concerns were flagged at the time of listing itself in financial press. When a stock makes its all-time high on day one and never returns to that level, that is the market telling you something clearly: this was priced too high for what the business actually is.

The Common Thread — What All These IPOs Got Wrong

Looking across all five cases, the pattern is identical every time. Overvaluation at issue price. Mechanical selling pressure when lock-ins expire. Governance or regulatory shocks that the IPO prospectus had quietly flagged as risks. And a profit story that kept getting pushed further into the future.

The mispriced certainty — of growth, of margins, of governance discipline, of regulatory safety — is what retail investors paid for. And when that certainty cracked, the repricing happened in days, not months.

Three Rules to Protect Yourself in Every Future IPO

One: Read the lock-in schedule before you apply, not after. Mark every date in your calendar. Treat each unlock as a potential supply event, especially if the stock has already run up.

Two: Demand a realistic profit timeline. If the company cannot tell you clearly when it will be consistently profitable — and by how much — the IPO price is probably pricing in hope, not reality.

Three: Separate the brand from the business. Paytm was a brand everyone knew. Ola was a brand everyone used. Brand familiarity is not a valuation argument. Always ask: at this price, what growth is already baked in?

India's IPO market will keep producing both winners and losers. The difference between retail investors who make money and those who lose it often comes down to whether they read the fine print — or just followed the hype.

Discussion 0

No comments yet

Be the first to share your thoughts!